Overview of the Vacation Rental Sector in Spain 2025: Trends, regulation, and opportunities by region

Angela Martínez

10 min

·

July 30, 2025

.png)

By 2025, vacation rentals in Spain have firmly established themselves as a cornerstone of the tourism industry, fueled by strong international demand, a more professionalized supply, and the intensive use of technology. Yet, the sector is navigating mounting regulatory challenges, particularly in major cities, which are giving rise to alternative models such as mid-term rentals. Its future will hinge on striking the right balance between profitability, compliance, and sustainability against a backdrop where large operators and digital transformation are shaping the competitive landscape.

This sustained demand directly fuels the vacation apartment rental market, especially in urban and coastal areas such as Málaga, Barcelona, and the Balearic Islands.

This growth not only reflects a post-pandemic recovery but also a new consolidation cycle driven by international tourism and the expansion of alternative accommodation models such as vacation rentals.

The supply of TUH properties continues to grow steadily.

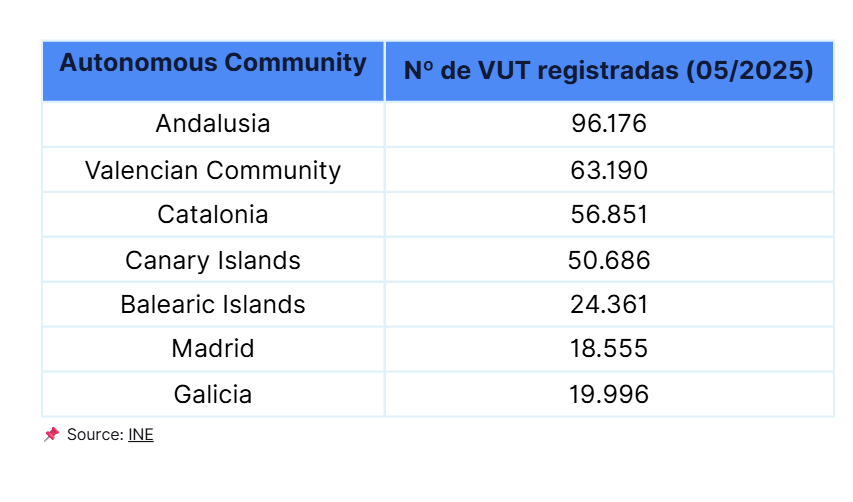

As of May 2025, Spain had 381,837 registered TUHs, an increase of +8% compared to 2024 (Source: INE).

This growth has led to increased regulatory pressure, particularly in urban areas with high population density and a shortage of long-term housing.

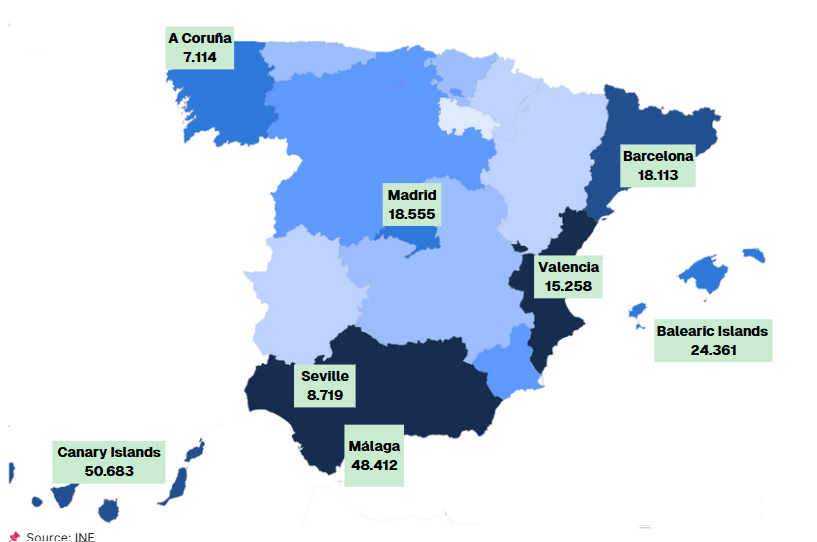

Regions such as Andalusia (96,176 TUHs), the Valencian Community (63,190 TUHs), and Catalonia (56,851 TUHs) lead in the number of vacation rental properties. Cities like Málaga (48,412 TUHs) and Barcelona (18,113 TUHs), as well as the Balearic Islands (24,361 TUHs) and the Canary Islands (50,686 TUHs), have experienced accelerated growth but also face urban planning and regulatory challenges.

This expansion is not uniform. Certain regions, such as Málaga or the Balearic Islands, have seen particularly sharp increases but also face mounting pressure to limit further growth.

Understanding the profile and behavior of TUH guests is essential for adapting supply. In 2025, the TUH guest profile includes:

Knowing these traits enables better marketing segmentation, dynamic pricing, and personalized services to attract bookings.

The TUH market is no longer dominated solely by small owners. Professional managers and institutional investors are playing an increasingly important role.

This shift could lead to sector consolidation, favoring the most tech-enabled and scalable operators, and increasing quality and compliance standards.

The vacation rental sector in 2025 is defined by five main transformation drivers:

Property owners have evolved from occasional hosts to micro-entrepreneurs in the accommodation business. Tools such as PMS (Property Management Systems), automated pricing managers, accounting software, basic utilities management platforms, and tourism CRMs enable scalable operations from the very first unit.

Technology is also enhancing the guest experience. From digital contract signing to chatbot-based support and remote door access, guests now expect a “contactless yet seamless” stay.

The average nightly rate for vacation rentals in Spain stands at €192 (Source: Holidu). Despite rising inflation, demand remains stable, although travelers are adjusting their habits: comparing more prices before booking, slightly shortening their stays, and showing increased price sensitivity.

Average stay length:

According to Beyond Pricing, the lead time—the average time between booking and guest check-in—currently stands at 29.5 days, a 9% year-on-year decrease.

This indicates a structural shift in guest behavior: last-minute bookings are on the rise, increasing the importance of real-time pricing adjustments to avoid revenue loss from poorly calibrated rates.

2025 marks a turning point with the implementation of the mandatory national TUH registry starting in July. In addition, cities like Barcelona, Palma de Mallorca, and San Sebastián are tightening license requirements, reducing capacity limits, and enforcing stricter technical and coexistence standards.

High-tourism pressure areas with strong profitability for vacation rentals include:

The tourist profile in these areas continues to be dominated by the international market, with the UK, Germany, France, and Italy accounting for over 54% of foreign demand.

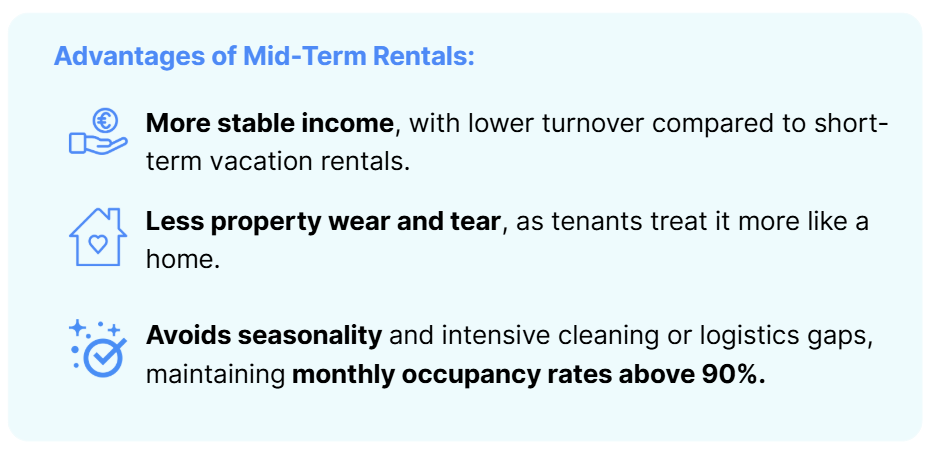

Mid-term rentals—contracts ranging from 1 to 6 months—are gaining relevance as a hybrid model between vacation and residential leasing, offering greater stability for owners and flexibility for tenants.

According to BrainsRE, this model is “shifting from being an intermediate solution to becoming a standalone business model.”

This trend is particularly strong in secondary and urban destinations with demand from digital nomads, relocated professionals, and short-season tourism (e.g., Málaga has seen a 37% increase in stays of over 20 nights during autumn and winter).

The distribution and booking management of TUHs is now almost fully digitalized:

This digitalization improves operational efficiency: from automatic calendar synchronization to automated guest communication and integrated accounting management.

The vacation rental market in Spain is entering a new stage of maturity. The combination of regulatory pressure, mandatory digitalization, demand segmentation, and industry professionalization is shaping a new competitive landscape.

Looking ahead to 2026, three likely scenarios emerge:

One thing is clear: vacation rentals are no longer an alternative—they are a consolidated industry that, to thrive, must find a balance between profitability, urban coexistence, and long-term sustainability.

Our service fees pay for themselves with the time and money saved by using Polaroo.