Disbursements: what they are, how to identify them and why proper accounting matters.

Diana Cifuentes

8 min

·

January 19, 2026

Confusing a disbursement with an expense can lead to accounting errors and penalties. We explain how to avoid this with a real example from a water bill.

In the management of a company’s utility supplies, not all the amounts shown on an invoice represent a real expense. This nuance, which may seem minor, has a direct impact on accounting, taxation and the overall profitability of the business.

Although the concept applies to different contexts, the water bill is one of the clearest examples for understanding what a disbursement is, how to identify it and why it is important to manage it correctly, especially in companies with multiple assets or locations.

A disbursement is an amount that a company pays on behalf of a third party and subsequently recharges at the same value, without applying any margin or profit.

From an accounting and tax perspective, a disbursement:

In this type of transaction, the company acts solely as a payment intermediary, not as the final consumer of the service.

In practice, disbursements often cause confusion because, at first glance, they appear to be just another expense item on the invoice. This usually happens for two main reasons.

First, disbursements are often integrated into the same invoice together with other items billed directly by the supplier, without a clear visual separation.

Second, invoices do not usually explicitly identify these amounts as “disbursements”. Instead, their nature must be inferred because the charge is issued in the name of a third party rather than the main service provider.

A very common example of this type of confusion can be found on water bills, where items such as fees, levies or sanitation charges are often considered disbursements, even though they are not always explicitly labelled as such.

The water bill is a particularly representative case for understanding how disbursements work in practice.

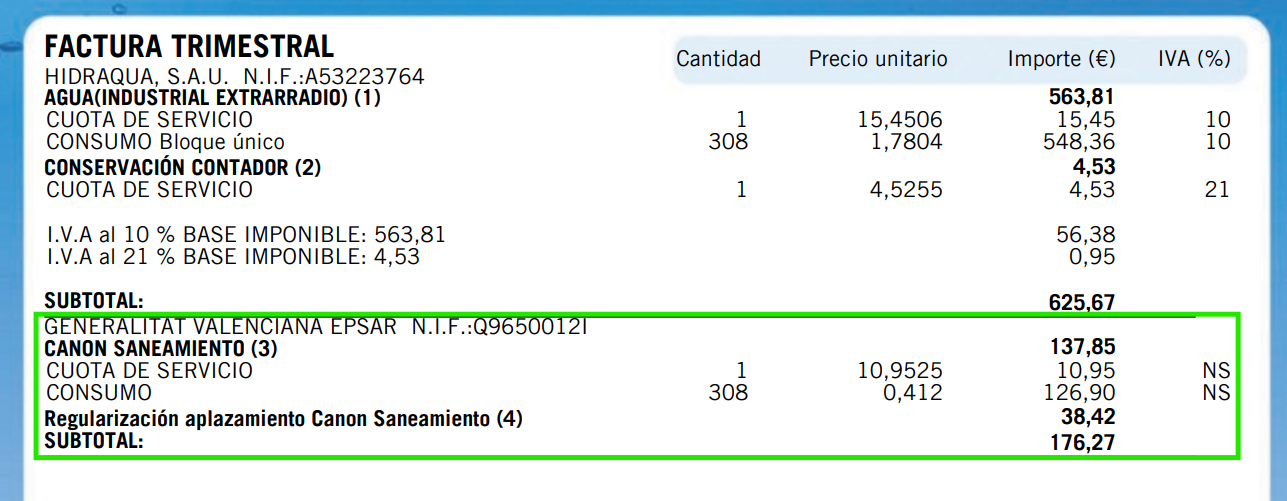

In a quarterly water bill, it is common to find different items such as the service charge, tiered consumption charges, meter maintenance, and the sanitation levy.

This levy is a clear example of a disbursement (known in Spanish as suplido), since the provider simply passes on to the customer an amount that actually corresponds to a third party. A key indicator is that it is not subject to VAT, as disbursements generally do not form part of the taxable base. In addition, the invoice must clearly identify the entity to which the amount is paid, since the supplier is acting solely as a payment intermediary.

Understanding this distinction is essential for correctly interpreting the invoice and for proper tax and accounting management of utility expenses.

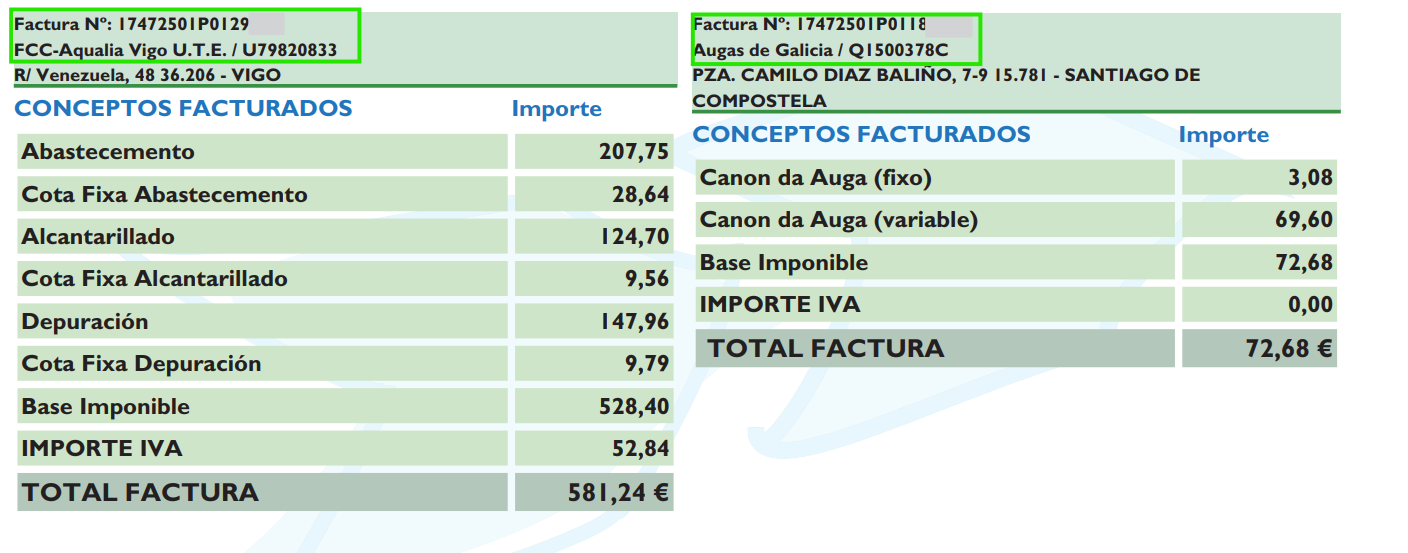

In some water bills, especially in large cities or metropolitan areas, items appear grouped under headings such as “Other environmental services”. This block is a clear example of disbursements, as it includes charges that do not correspond directly to the water supply company, but to various public entities.

In this case, all of these amounts are considered disbursements, since the company managing the invoice acts solely as a payment intermediary.

Within the “Other environmental services” category, you may find, for example:

Although all these amounts appear grouped on a single invoice, each one corresponds to a different issuing entity and to a specific service linked to the integral water cycle.

These charges meet all the conditions required to be considered disbursements:

In addition, on the invoice itself:

This last point is particularly relevant, as it shows that a single document may include several disbursements, even when payment is made in a consolidated way.

Not all charges issued by another entity are necessarily disbursements. If an item, even if it comes from a third party, appears under a different invoice number, it is considered a separate transaction and must be accounted for independently.

This means that, in order to correctly identify a disbursement, in addition to reviewing the tax ID, VAT and description, you must also check whether it shares the same invoice number as the supplier’s own services.

A water bill usually includes different items. Identifying them correctly is key.

These amounts can be treated as disbursements provided they are issued by a third party, are not subject to VAT and do not correspond to services directly supplied by the main service provider.

Poor management of disbursements on invoices can generate several problems, especially when the volume of invoices is high.

❌ Tax errors

❌ Incorrect taxable bases

❌ Distorted profitability

❌ Lack of cost control

❌ Risks during audits or inspections

When a company manages dozens or hundreds of water bills:

Manually distinguishing disbursements from own expenses not only consumes time, but also increases the risk of costly errors and delays decision-making.

With Polaroo, identifying and managing disbursements stops being a manual task and becomes an automatic, reliable and fast process:

In 2025, 6% of all water bills managed for our clients corresponded to disbursements. Polaroo detected them automatically, without any manual intervention, ensuring that no tax or accounting errors went unnoticed.

Companies that do not use Polaroo are incurring hidden costs and significant time losses:

💡 In other words: every invoice that is not processed with automation represents lost time and money. Polaroo turns a manual, error-prone process into a 100% automated, reliable and traceable workflow, reducing operational costs and tax risks.

A disbursement is not a minor detail or a mere accounting technicality: it is a key element in ensuring correct tax, accounting and financial management. The water bill is one of the most common — and at the same time most complex — examples of how a single document can include both real expenses and amounts that the company only advances on behalf of third parties.

In companies with multiple assets or locations, where invoice volume and the diversity of items multiply, this distinction stops being operational and becomes strategic. Without structured data and proper traceability, disbursements are diluted within expenses, leading to inefficiencies and decisions based on incomplete information.

For this reason, professionalising the management of disbursements — especially in utilities such as water — not only improves regulatory compliance, but also provides control, clarity and analytical capability. In this context, having technological tools that automate the identification and treatment of these items makes a real difference in cost management and in the quality of financial information.

Our service fees pay for themselves with the time and money saved by using Polaroo.